Introduction

A single CNC machining center, vertical turret lathe, or horizontal boring mill can cost anywhere from $75,000 to well over $500,000. For manufacturers of all sizes, tying up that much working capital in one purchase puts enormous strain on day-to-day operations, restricts growth opportunities, and limits flexibility to respond to new orders or market shifts.

In 2026, reshoring initiatives, advanced manufacturing incentives, and accelerating automation are pushing equipment investment higher across aerospace, medical device, and precision manufacturing. According to the Equipment Leasing and Finance Association, the U.S. equipment finance industry reached $1.34 trillion in 2023, with 82% of businesses using some form of financing to acquire equipment rather than paying cash.

This guide breaks down every major financing option — conventional equipment loans, operating leases, SBA programs, and sale-leaseback arrangements — along with qualification requirements, 2026 tax incentives, and practical guidance to help manufacturing businesses make cost-efficient financing decisions.

Key Takeaways

- Industrial equipment financing lets manufacturers acquire expensive machinery through loans, leases, SBA programs, or sale-leaseback arrangements without large upfront cash outlays

- Typical requirements: 600+ credit score, 1–2 years in business, basic financial documentation; used equipment is also financeable

- Section 179 ($2.56M cap) and restored 100% bonus depreciation can sharply cut effective cost for machinery placed in service by year-end 2026

- Terms run 24–84 months; shorter terms mean higher payments but less interest, longer terms preserve cash flow

- Compare at least three lenders before committing — a specialized machine tool dealer can help you identify financing options suited to the equipment you're buying

What Is Industrial Equipment Financing?

Industrial equipment financing is a category of business lending in which a lender provides capital specifically to acquire machinery or equipment. The equipment itself typically serves as collateral, which results in more favorable interest rates and approval terms than unsecured loans.

Two Broad Structures: Loans vs. Leases

Equipment Loans:

- Business eventually owns the equipment outright

- Asset appears on balance sheet

- Eligible for Section 179 and bonus depreciation

Equipment Leases:

- Business pays for use over a term (24–60 months)

- Options at end: buy, return, or upgrade

- Operating leases keep equipment off balance sheet

- Finance leases function more like loans with $1 buyout

The distinction carries real cash flow, balance sheet, and tax consequences — worth working through with an accountant before committing. That said, the structure you choose matters less than understanding why industrial equipment lends itself to financing in the first place.

Why Industrial Equipment Is Ideal for Financing

Compared to consumable business expenses, industrial machine tools are particularly well-suited to financing:

- Boring mills, turret lathes, and grinders routinely stay productive for 15–30 years — long enough that financing the purchase makes economic sense

- Precision equipment from established brands like FEMCO, Webster & Bennett, and Clausing holds its value well, giving lenders confidence in the collateral

- Lenders can directly tie the machine to billable production, making underwriting more straightforward than with general business expenses

Taken together, these characteristics explain why equipment-secured deals often come with lower down payments and longer repayment windows than general business loans.

Financing Options for Industrial Equipment in 2026

Equipment Loans (Conventional Financing)

A conventional equipment loan works like this: the lender advances the purchase price, the borrower repays in fixed monthly installments over an agreed term (typically 24–84 months), and ownership transfers immediately or at loan payoff.

Key features:

- Down payments of 10–20% are common, though 100% financing is available for qualified borrowers

- Fixed-rate structures provide payment predictability, which matters for manufacturers managing project-based cash flow

- Full ownership from day one means immediate depreciation and Section 179 deductions

This structure works best for businesses with strong credit profiles that want to build equity and maximize tax benefits — particularly for long-lived assets like boring mills or engine lathes.

Equipment Leases: Operating vs. Finance (Capital) Lease

Operating Lease — the lessor retains ownership while your business uses the equipment for a set term (often 24–60 months):

- End-of-term options: return, renew, or purchase at fair market value

- Payments are often fully deductible as operating expenses

- Best fit for technology-forward equipment that may become obsolete, such as CNC controls or software-driven systems

Finance (Capital) Lease — structured more like a loan, with ownership transferring to the business:

- Asset goes on your balance sheet; you claim depreciation

- Typically ends with a $1 buyout or fixed nominal purchase price

- Best for equipment you intend to own long-term, such as vertical turret lathes or horizontal boring mills with 20–30 year useful lives

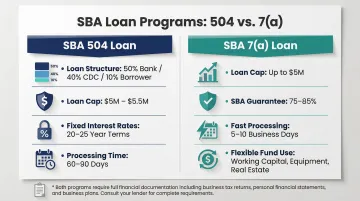

SBA Loans: 7(a) and 504 Programs

SBA 504 Loan:

The SBA 504 programis the gold standard for large industrial equipment purchases. A Certified Development Company (CDC) partners with a conventional lender to fund up to 90% of the project cost at long, fixed terms.

Loan structure:

- 50% conventional bank loan (first lien)

- 40% CDC/SBA debenture (second lien)

- 10% borrower equity (down payment)

2026 limits and rates:

- $5 million standard loan cap

- $5.5 million for small manufacturers

- 20-year fixed debenture rates: 5.91%–5.98% (April 2026)

- 25-year fixed debenture rates: 5.85%–5.94% (April 2026)

Requirements to keep in mind:

- Equipment must have a 10+ year useful life

- Approval and processing typically take 60–90 days

- Extensive documentation required

The 504 is purpose-built for heavy capital expenditures. For businesses that need more flexibility — or want to bundle equipment with installation costs — the 7(a) program is worth considering.

SBA 7(a) Loan:

The SBA 7(a) program offers more flexibility than the 504. It can cover equipment within a broader working capital package — useful for businesses needing to finance both equipment and associated installation, tooling, or facility modifications simultaneously.

Key details:

- Maximum $5 million loan amount

- SBA guarantees 75%–85% of the loan

- Faster processing: 5–10 business days (standard); 24 hours through the Preferred Lender Program (PLP)

- More flexible use of funds than the 504

Note: Both SBA programs require more documentation and longer processing times than conventional loans. Factor this into your project timeline, especially if you need equipment placed in service by December 31 for tax purposes.

Sale-Leaseback

A sale-leaseback allows a manufacturer to sell equipment it already owns to a finance company and immediately lease it back. This frees up cash from existing assets while operations continue uninterrupted.

This option works well for:

- Shops with aging machinery on the books that need cash for expansion

- Businesses looking to fund a new equipment purchase using existing assets

- Manufacturers needing working capital without taking on new debt

The transaction creates immediate liquidity without disrupting operations. However, you'll pay interest on equipment you previously owned outright, so calculate the total cost carefully.

Vendor and In-House Financing

Some machine tool dealers and manufacturers offer in-house financing or preferred lending partnerships. For example, working with a specialized dealer — such as T.R. Wigglesworth Machinery Company, which has carried both new and pre-owned machine tools since 1935 and is an authorized dealer for brands including FEMCO, KENT, and DAH LIH — can simplify the purchase process and occasionally provide promotional rates.

Advantages include:

- Single point of contact for both equipment selection and financing

- Dealer relationships with lenders who understand equipment values and resale

- Occasional promotional rates (0% for a set period, deferred payments)

One practical note: always compare vendor-offered terms against independent lender quotes before committing. Dealer rates aren't automatically better, and going in with competing offers preserves your negotiating leverage.

What Industrial Machine Tools Can Be Financed?

Virtually any revenue-generating industrial asset qualifies for equipment financing:

Commonly Financed Equipment:

- CNC machining centers (horizontal and vertical)

- Vertical turret lathes (VTLs)

- Horizontal and vertical boring mills

- Surface and cylindrical grinders

- Jig borers

- EDM machines

- Automated production cells

- Fabricating equipment (press brakes, plasma cutting tables, ironworkers)

Lenders assess three key factors when evaluating a financing application:

- Useful life — how long the asset will remain productive

- Resale value — what the equipment is worth if the borrower defaults

- Revenue-generating capacity — whether the machine directly supports billable work

Precision machine tools from established manufacturers score well on all three.

Used Industrial Equipment Is Also Financeable

Lenders generally require an independent appraisal or a dealer invoice to establish fair market value. Equipment in good working order from reputable brands (Webster & Bennett, FEMCO, Clausing, Kent) tends to qualify without issue.

That said, used equipment financing comes with adjusted terms:

| Factor | New Equipment | Used Equipment |

|---|---|---|

| Loan-to-Value (LTV) | Up to 90% | 60–85% |

| Down Payment | 10–15% | 15–25% |

| Appraisal Requirement | Generally not required | Required |

LTV floors toward 60% when equipment is older, has high hours, or lacks documentation of recent service history — so condition records matter before you apply.

Soft Costs Can Be Rolled Into Financing

Delivery, installation, operator training, tooling packages, and software licenses can sometimes be included in the financing package. This avoids a large cash outlay at startup and keeps the total financed cost in a single monthly payment. Not every lender allows soft cost roll-ins, so it's worth asking upfront — and comparing offers from lenders who do against those who don't.

How to Qualify for Industrial Equipment Financing

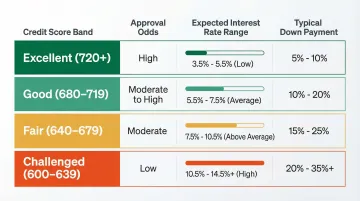

Lenders evaluate several factors when reviewing an equipment financing application — credit profile, business history, financials, and the equipment's value all factor into the decision. Here's what to expect across each area.

Credit Profile

Most conventional lenders look for a business credit score or personal guarantor score of at least 600–650. SBA programs may require higher (680+).

Lower scores don't automatically disqualify you. Lenders consider:

- Equipment's collateral value

- Business cash flow strength

- Presence of other collateral

- Down payment size

According to equipment finance specialists, alternative lenders will finance scores as low as 600 if Debt Service Coverage Ratio (DSCR) is strong and a 20–25% down payment is provided.

| Credit Score | Approval Odds | Expected Interest Rates | Typical Down Payment |

|---|---|---|---|

| Excellent (720+) | Best rates | 7–9% | 10–15% |

| Good (680–719) | Competitive | 9–11% | 10–15% |

| Fair (640–679) | Moderate | 11–13% | 15–20% |

| Challenged (600–639) | Alternative lenders | 12–15% | 20–25% |

Time in Business

Most conventional lenders prefer 2+ years of operating history. Some alternative or online lenders work with businesses as young as 6–12 months, often with higher rates or down payment requirements.

Startups should expect more scrutiny and may benefit from an SBA program or a lender with a dedicated startup financing program.

Financial Documentation

Lenders typically request:

- Last 2–3 years of business tax returns

- Year-to-date profit and loss statement

- Current balance sheet

- 3–6 months of business bank statements

- Equipment invoice or quote (with specs)

- Personal financial statements from guarantors (for larger loans)

Having these documents organized before you apply speeds up approval and reduces back-and-forth with the lender.

Debt Service Coverage Ratio (DSCR)

DSCR measures whether your business generates sufficient net income to cover the new payment obligation. It's calculated as:

DSCR = Net Operating Income ÷ Total Annual Debt Service

Example:

- Annual net operating income: $250,000

- Existing annual debt payments: $80,000

- New equipment loan annual payment: $60,000

- Total annual debt service: $140,000

- DSCR = $250,000 ÷ $140,000 = 1.79

Most lenders require a minimum DSCR of 1.25x. For SBA 7(a) Small Loans, the requirement is 1.10x (effective March 2026).

Down Payment and Collateral

Typical down payment: 10–20% of equipment cost 100% financing: Available for borrowers with strong credit profiles (720+)

Key collateral considerations:

- The equipment itself serves as primary collateral in most deals

- Larger transactions ($250,000+) may trigger a blanket lien on business assets

- You can negotiate to exclude the blanket lien requirement — many lenders will accept this for qualified borrowers

Tax Advantages and 2026 Market Considerations

Section 179 Deduction

Under Section 179, a business can deduct the full purchase price of qualifying equipment placed in service during the tax year, up to the annual deduction limit.

2026 Limits:

- Maximum deduction: $2,560,000

- Phase-out threshold: $4,090,000

- Deduction reduces dollar-for-dollar once total equipment purchases exceed $4.09M

Critical points:

- Applies whether equipment is purchased outright or financed

- Tax benefit available even if only a small down payment was made

- Equipment must be purchased AND placed in service before December 31

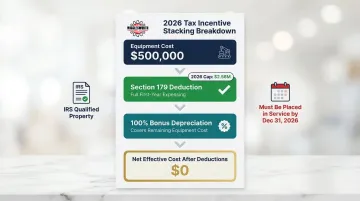

Bonus Depreciation

The One Big Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025.

For 2026, that translates to:

- An additional 100% first-year depreciation deduction on eligible equipment

- Coverage for both new and used equipment

- Combination with Section 179, subject to taxable income limitations

Example:

- $500,000 CNC machining center purchased and placed in service in 2026

- Section 179 deduction: $500,000 (full cost)

- Bonus depreciation: Not needed if Section 179 covers full amount

- If equipment exceeds Section 179 cap or taxable income limitation, bonus depreciation covers the remainder at 100%

Run these numbers with your CPA — the interaction between Section 179 and bonus depreciation varies by taxable income and total equipment spend.

2026 Market Trends to Factor In

Interest Rate Environment

The Federal Reserve held the target rate at 3.50%–3.75% in March 2026, with the median projection at 3.1% by year-end. Borrowing costs are stabilizing after years of volatility — which shapes how you should structure your financing:

- Expecting further rate cuts? Choose shorter terms (36–48 months) to refinance at lower rates sooner.

- Want payment certainty? Lock in a 5–7 year fixed rate now before projections shift.

Reshoring and Industrial Demand

U.S. manufacturing reshoring and foreign direct investment job announcements reached 244,000 in 2024. That expansion has driven machine tool demand to record levels — new orders of metalworking machinery hit $814.3 million in December 2025, up 59.9% year-over-year.

The practical consequences for buyers:

- Increased competition for available industrial equipment

- Longer lead times, especially for CNC machining centers and VTLs

- Pre-approved financing gives you negotiating leverage with dealers

Tips for Securing the Best Industrial Equipment Financing Deal

Compare Multiple Lenders Before Committing

Obtain quotes from at least three sources:

- Regional bank (relationship lending, local decision-making)

- SBA-approved lender (long terms, low rates, higher documentation)

- Specialty equipment finance company (understands manufacturing, flexible underwriting)

The equipment finance market is fragmented — rates and structures can vary significantly for the same credit profile. Lenders that specialize in manufacturing or heavy equipment will often underwrite deals that generalist lenders decline.

Know Total Cost, Not Just Monthly Payment

Advertised interest rates don't tell the full story. Calculate effective APR once all fees are included:

- Origination fee (1–5% of loan amount)

- Documentation fee ($250–$500)

- UCC filing fee ($50–$150)

- Appraisal fee (for used equipment: $500–$2,000)

Example:

- Loan amount: $300,000

- Stated rate: 8.5% over 60 months

- Monthly payment: $6,137

- Origination fee (3%): $9,000

- Documentation fee: $400

- Effective APR: 9.2%

Request an amortization schedule and calculate total interest paid over the term before deciding between a shorter, higher monthly payment and a longer, lower monthly payment structure.

Time the Purchase Around Tax Deadlines

Equipment must be purchased AND placed in service before December 31 to qualify for Section 179 in that tax year. Factor in:

- Vendor lead times (4–16 weeks for new equipment)

- Lender processing time (7–90 days depending on program)

- Delivery and installation schedules (1–4 weeks)

Timeline example for year-end 2026 purchase:

- October 1: Begin lender applications

- October 15: Select lender, submit full documentation

- November 1: Approval and closing

- November 15: Place equipment order

- December 15: Delivery and installation

- December 20: Equipment placed in service (eligible for 2026 Section 179)

Pre-approval before finalizing the equipment choice prevents delays that could push a purchase into the next tax year.

Negotiate Soft Costs Into the Financing Package

Delivery, installation, training, and tooling are often financeable when bundled with the equipment purchase. Rolling these into the loan avoids a large cash outlay at startup and keeps the total financed cost in a single monthly payment.

Example:

- CNC machining center: $350,000

- Delivery and rigging: $8,000

- Installation and alignment: $12,000

- Operator training (3 days): $5,000

- Initial tooling package: $15,000

- Total financed: $390,000

Not all lenders allow this — ask upfront and use it as a negotiating point when comparing offers.

Build and Protect Business Credit Before Applying

90 days before applying:

- Pay down revolving credit lines (reduces debt-to-income ratio)

- Ensure no derogatory marks appear on business credit reports

- Avoid new credit applications (hard inquiries lower scores temporarily)

- Verify business credit reports are accurate (Dun & Bradstreet, Experian Business, Equifax Business)

A clean payment history on previous equipment loans strengthens the application considerably — and may yield lower rates or eliminate down payment requirements entirely.

| Product | Product Details |

|---|---|

| HL-250 | Explore Product |

| BMC-110R1 | Explore Product |

| 3VS08 - Clausing Knee Mill 54" Long x 10" Wide Table | Explore Product |

Frequently Asked Questions

What credit score do I need to finance industrial equipment?

Most conventional lenders require 600–650+, and SBA programs may require 680 or higher. However, a strong equipment profile and business cash flow can partially offset a weaker credit score, especially with alternative lenders who focus on DSCR rather than credit alone.

Can I finance used industrial machine tools?

Yes. Used equipment is financeable, though lenders typically require an appraisal or dealer invoice to establish value. Well-maintained machines from established brands (FEMCO, Clausing, Webster & Bennett) generally qualify without issue, though LTV caps may be lower (60–85% vs. 90% for new equipment).

What is the difference between an equipment loan and an equipment lease for industrial machinery?

A loan transfers ownership to the borrower from the start and builds equity, allowing immediate depreciation and Section 179 deductions. A lease provides use of the equipment for a term with options to buy, return, or upgrade, with balance sheet and tax treatment varying depending on whether it's an operating or finance lease.

How long are typical repayment terms for industrial equipment financing?

Terms typically range from 24 to 84 months (2–7 years). Heavy industrial machinery sometimes qualifies for longer terms due to its extended useful life.

Does Section 179 apply to equipment purchased through financing?

Yes. Section 179 applies to financed equipment as long as it is placed in service within the tax year. The full deductible amount is not limited to the down payment made — you can deduct the entire purchase price even if you financed 100%.

How much down payment is typically required for industrial equipment financing?

Most lenders require 10–20% down, though 100% financing is available for borrowers with strong credit (720+) and established business history (typically 2+ years). Some SBA programs can finance up to 90% of the total project cost with no traditional down payment, though a 10% equity injection is required.